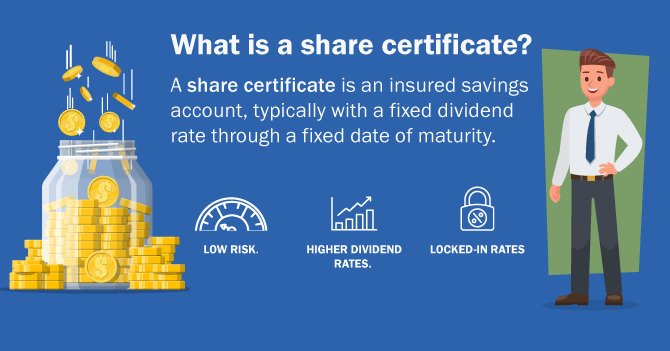

What is a share certificate?

A share certificate is an insured savings account, typically with a fixed dividend rate through a fixed date of maturity. A share certificate from a credit union is similar to a certificate of deposit, or CD, from a bank. These accounts offer highly competitive rates by locking your funds into a fixed term. For example, USALLIANCE offers Certificate Accounts ranging from 3 to 60 months in term. The rate is different for different term lengths, but you can choose the rate and term combination that works the best for your financial situation.

What are the advantages of share certificates?

- Low risk. Your money is safe in a share certificate account, as they are considered among the lowest-risk investment options available. As long as your share certificate is insured by the NCUA, then your money is protected up to $250,000. There are rare circumstances where you can lose money if you invest over $250,000 or are invested in a certificate is not insured by the NCUA, but most standard share certificates are considered one of the safest investments you can make.

- Higher dividend rates. While certificates offer the safety of a savings account, they offer much more upside in terms of returns on your deposit. The national average yield for savings accounts is 0.56% APY as of Jan. 4, 2024, according to Bankrate. Compare that to certificates that can have rates over 5.00% APY and it’s not difficult to see how a certificate share could boost your savings more.

- Locked-in rates. With a certificate, you don’t need to keep an eye on the market or be prepared to move money around to try to maximize your return. The APY* on a certificate is locked in until its maturity date, so there’s nothing you need to do but sit back and watch your savings grow!

What certificate term should I choose?

When you open your certificate, you’ll be given a choice for the maturity term. Your options will typically range between three and 60 months, with different rates offered for different terms. As a general rule of thumb, certificates with longer maturity terms will earn a higher rate, but this is not always the case and rate should not be your only point of consideration.

While there is little monetary risk to your funds when they are locked into a certificate, it’s important to consider opportunity risk if you’re not able to access that money for a significant period of time. If there is a chance that you’ll need the money that you’re funding your certificate with in the near future, choosing a shorter term may be beneficial to you, even if your rate is not as high. Conversely, if the funds you’re using for your certificate are extra money or money you otherwise won’t need to access anytime soon, then choosing a longer term might be a good option for you to maximize your return.

In addition to rate and term, also factor the impact of your certificate(s) on your overall savings plan. Is that money being locked up going to put you in a difficult position? Do you have an emergency fund available outside of the money that is going into your certificate? Are there major expenses on the horizon you may need that money for? Consider all aspects of your financial situation before you choose how much to put into a certificate, and for how long.

How do I calculate the earnings on my share certificate?

Use this formula to calculate the earnings on your share certificate:

APY= (1 + r/n )^ n – 1

In this formula, “r” is the annual dividend rate and “n” is the number of compounding periods each year. Your share certificate can be compounded yearly, quarterly, monthly or daily, so be sure to check with your credit union when completing this formula.

Example: Where Rate (r) is 3.5% and number of periods (n) is 12

APY= (1 + r/n )^ n – 1

APY = [1 + (3.5% ÷ 12)] ^ 12 – 1

APY = 3.56%

Comments